It’s been a productive period for Raba and our portfolio, with many of our companies reporting strong year-to-date operating results in 2025. We appear to be emerging from the “fintech winter” — with several fintech IPOs this year and others waiting in the wings. Is this a sign of thaw? Maybe, but it’s important to examine the context and the factors driving fintech economics.

There are two factors behind the significant upside for fintechs:

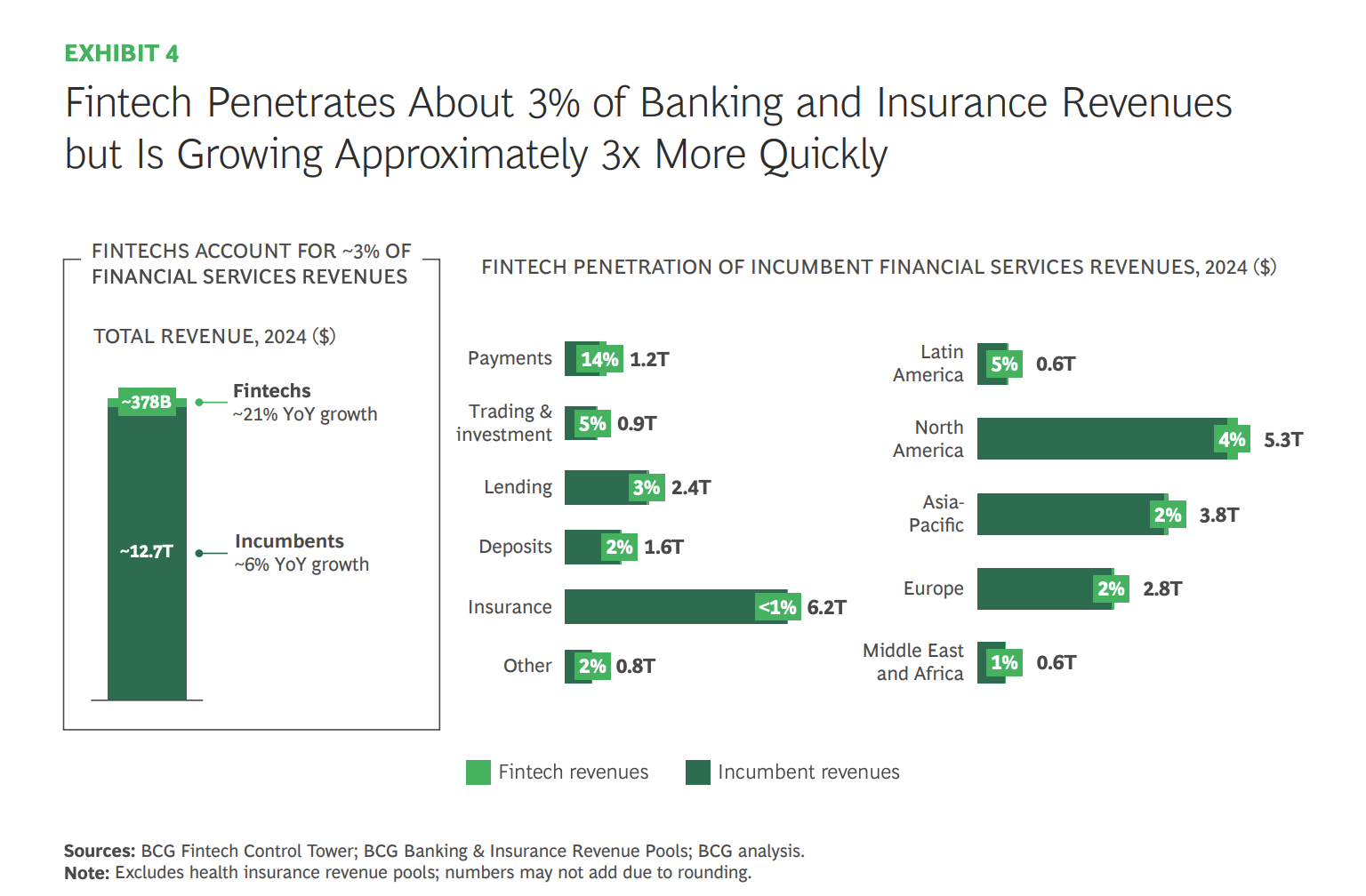

- Fintechs globally make up only 3 percent of global financial services revenues.

- Fintechs are gaining ground, growing more than 3x faster than incumbents.

To frame the opportunity, in Africa and the Middle East, financial services revenues amount to $600B per year and fintechs make up less than 1%. In Latin America, which has had a head start in capital formation, fintechs represent 5%. Additional details from the QED/BCG report are below.

Fintech funding rounds were down 13% in 2024 vs. 2023 after declining 51% in 2023 vs. 2022. Amidst this fintech winter, our fintech companies have not just survived, they have thrived. They’ve emerged more resilient, more focused, more profitable and in stronger competitive positions. Raba has become sharper in our focus and better equipped to help our founders both weather the harsher periods and capture the advantage when opportunities are asymmetrically in our favor (let’s see if this shows up in our 2025 NPS score!).

Our founders have had a particularly robust fundraising period these last few quarters, with 58% of Raba 1 and 84% of Raba 2 companies (by net asset value) raising priced institutional rounds since Q4-24. Valuations have reflected their progress, and financings have been completed with no “special terms”. We have five additional companies working toward closing funding rounds, which will take those numbers up to 72% and 92%, respectively. Securing high quality sources of follow-on capital has been challenging in this environment, and our founders have been resourceful and persistent in the effort, while not losing operating momentum. These rounds happen because of two consistent ingredients: 1. growth, and 2. a durable business model. These founders continue to build value, and we have high expectations for what they will build over the long term.

We need IPOs, man!

On our recent partnership call, we shared the state of at-scale African fintechs and their paths to IPOs (if you were unable to join, send us a note and we can share a recording). The two questions we addressed were what scale do you need to have a successful IPO and are there companies in Africa that fit the bill? The short answer to the second is yes. There are a crop of companies that have scale — $300M in annual revenue, 30% year-over-year dollar revenue growth and attractive business models (high margins, durability) — and these are companies that have counterparts in other markets that have gone public. Most companies that fit these criteria are fintechs and earn through a combination of transaction revenue, credit (lending revenue), and float (deposit revenue).

As we have seen across various businesses, it matters little where you start, but where you end up. Over the arc of time, fintechs will generally acquire licenses that give them bank-like capabilities to take on the largest financial services profit pools that have traditionally been claimed by banks. Evidence of this is Coinbase and Stripe pursuing banking charters.

To help frame the scale needed to IPO, below are data points for a 2025 crop of fintechs — Klarna, Chime and Circle — that have either filed S-1s or plan to:

- Scale: >$1B in annual revenue.

- Growth: from 15 - 30% YoY.

- Capital: collectively the three companies raised over $7B!

- Profitable? Not really … or barely.

- Tenure: all have been building >12 years, Klarna for over 20 years!

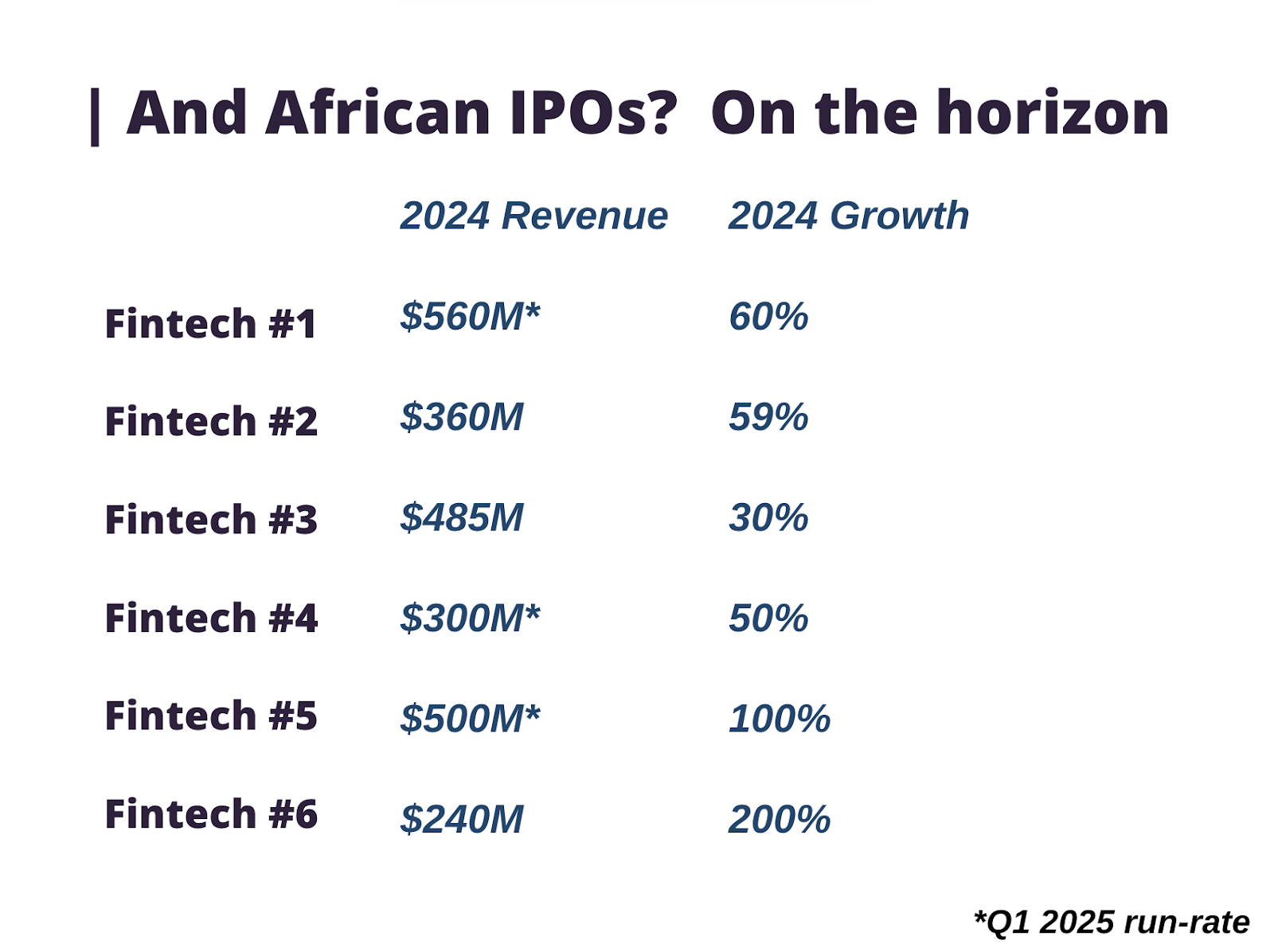

Most African fintechs haven’t yet had the benefit of compounding (15-20 years of build time), but we expect strong IPO contenders in the years ahead. Below is a table of African fintechs that have the “goods”. Even if you mark down forward growth to 20% in 2028, three of the five will generate greater than $1B in annual revenues, and we believe that yardstick along with growth and attractive business models are the pathway to an IPO.

Why does this matter?

The combination of scale and a clear path to public markets remains the engine that drives the venture capital model. While secondaries and continuation funds provide liquidity alternatives, the most significant pools of capital are unlocked in IPOs and acquisitions. Perception and psychology matter here — especially for African companies. Imagine a conversation in Menlo Park, London or New York about investing in a high-growth fintech on the continent. One of the first questions asked will be: what outcomes has the region produced? What are growth rates, margin structures, and valuation benchmarks? Do scaled fintechs trade at five times earnings or twenty-five? The answers will determine how investors engage.

Most of the at-scale companies are either listed on local exchanges with limited coverage or obscured inside large corporations like telecoms — businesses global investors haven’t heard of or spent time with. As a result, these companies often fall into the "too complicated" bucket. And in a market where AI businesses are scaling at unprecedented speed, it's even harder for fintech companies from too-hard-to-understand non-core geographies to capture global investor attention. That creates a short-term structural opportunity, as all of the (well-deserved) attention on AI tends to pull capital and mindshare away from other areas like Africa.

The fintech businesses referenced above will continue to grow, scale and offer a window into the broader potential of companies from the continent. As they approach public markets, US investors — increasingly represented on cap tables — will play a key role in shaping narratives, connecting companies to institutional capital, and fueling the information flywheel. But none of this happens without fundamental growth. Revenue and profit come from increased business activity and rising consumer wealth. For Africa, a key input to that equation is China.

China is a prime ingredient — but competition matters

A vibrant and upwardly mobile African consumer class is a long-term tailwind for China. Over the past 15 years, China has made significant investments in Africa and scaled trade partnerships to levels that now rival major global corridors. In 2024, China-Africa trade hit $295B — roughly 51% the size of China-US trade. Two decades ago, that figure was just 13%.

India and Middle Eastern economies (GCC) are now following a similar path. India and the GCC trade with Africa exceeded $300B in 2024. As mentioned in our partner call, Indian business and political leaders are leaning in:

- UPI (India’s real-time payments rail) is being rolled out in Ghana and Namibia, with several others in discussion.

- Airtel is investing $750M in capex across the continent.

- Earlier this year, India led its largest-ever joint naval exercise with African countries.

These are the capital lanes that will shape the continent. We believe they will become more competitive — and more valuable — over the next decade. For additional context, we’ve included a short video from our partner presentation that outlines the China/India-Africa trade arc here.

The equation: population x infrastructure x competition

The math is simple: massive population growth, accelerating infrastructure investment, and a steady decline in the cost of technology lead to innovation and new business opportunities. Smartphones that cost $500 a decade ago now sell for $80–100. Competition across the Global South to serve Africa’s emerging middle class is intensifying — and for the first time in modern history, the continent has multiple credible partners. Europe and the U.S. are trying to curb China’s influence due to growing trade deficits (Europe’s trade deficit with China grew from €110 billion in 2014 to over €300 billion in 2024), as they see these imbalances impacting supply chains, national security, and local economies.

Of course, there are unknowns. Much of today’s China/Africa trade is concentrated in resources and infrastructure — roads, ports, bridges — which don’t translate into local jobs or improved services. The question is how governments will respond. Will they structure these deals to prioritize employment and strengthen education, healthcare and digital capacity?

From a technology perspective, AI-native tools like ChatGPT introduce real leverage. A student can now build a custom tutor in minutes. A government could deploy LLMs to address teacher shortages at national scale. What are the long-term implications of this shift? Whatever they are, we believe they point to upward change. These are the structural tailwinds that will define Africa’s next chapter — and they create significant momentum for the continent’s digital champions, particularly in financial services.